58

FINANCEREPORTUNITEDACQUISITION

IRNAPRIL-MAY 2014

National Pump - estimatedgrowth

Agooddeal?

U

nited’s press release on the National Pump

acquisitionusedcarefullychosenwords. The

first sentence focused on “financial returns

throughout the cycle” which shows a desire for

United not to be seen as a cyclical rental company

tied to the peaks and troughs of construction.

Fifty percent of National’s revenue comes from

the energy sector. National Pump was founded in

2007, and United Rentals was happy to report it has

grown at over 50% per year since 2010. United’s

ownbusiness is growing at around6 to 7% a year.

In the ‘Private Equity Wakes Up’ article in

IRN’s

February 2014 issue, nearly all the recent private

equity acquisition analyses disclosed very little

information, sometimes not even the acquisition

value. As United Rentals’ shares are traded on the

New York Stock Exchange it hasmany investors and

has tomaintain its credibility with these owners. It

has also had its own ups and downs in the past: in

2008 it famously wrote off more than US$1 billion

in acquisition goodwill. This makes both United

and its shareholders wary of overpaying for rental

company acquisitions.

Valuationmethods

The enterprise valuation method makes it easy

to compare different rental companies with

different depreciation policies and debt levels.

Most other valuation methods focus on profit, but

in rental businesses profit is heavily influenced by

depreciation policy and the replacement cycle for

rental fleet.

A company is more valuable the higher its

cashflow, provided it can handle its debt. The

enterprise value of a company is a multiple of the

operating cash flow (Earnings Before Interest Tax

Depreciation Amortisation or EBITDA). The price to

acquire a company is usually the enterprise value

minus its debt. The equipment lease portion of a

company’s debt usually continues with the new

owner.

EBITDA multiples range from perhaps three

to nine, depending on the growth rate and cash

generation capacity of the company, its market

position and desirability, and the certainty of its

growth and cashflow.

In good times, before the 2008 financial crisis,

many acquisitions of rental companies seemed to

average six times EBITDA minus debt. Why six and

not four, or eight?

The banks seemed to be able to handle four times

EBITDA as the loan to acquire the company, so an

equity investor could buy a business using this loan

plus another two times EBITDA. This worked fine as

longasdebtwasavailable, and the companies could

profitably, reliably 'outgrow their debt' withgrowing

cashflow.

National financials

Unusually in this case, United has given

information, includingNational Pump’s2013 revenue

($211 million), historical growth (50% per year

from 2010 to 2013), EBITDA at 49% of revenue,

and even the relationship between rental revenue

and equipment original cost (dollar or financial

utilisation at 80%). Very unusually, United has

said it has “plans to double the size of the pump

business in five years.”

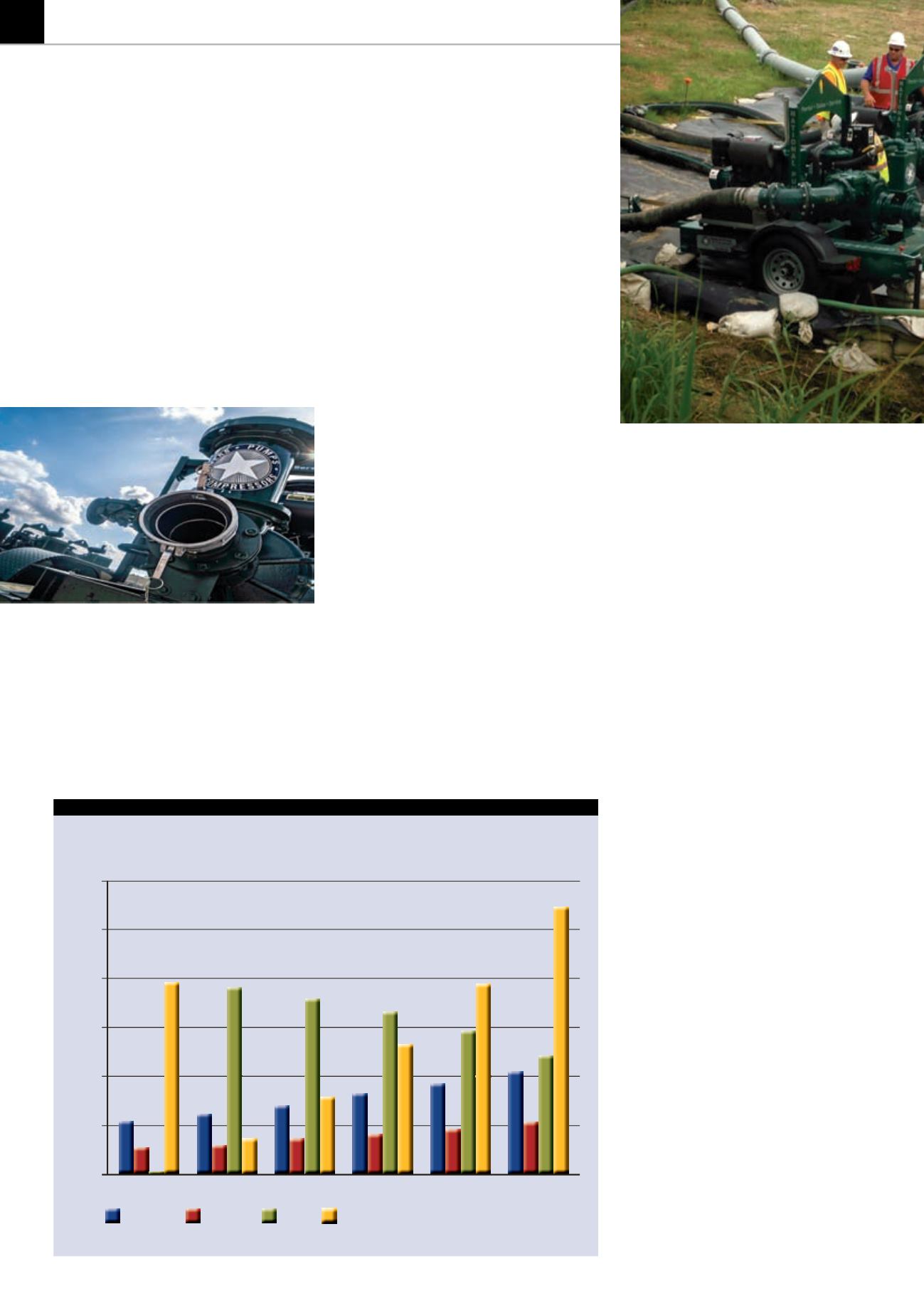

If we project the value of the acquired company

on today’s profitability, dollar (financial) utilisation,

at the “double in five years” growth rate, which is

around 15% compound per year, we can try to see if

the companywill grow in value (see graphon left).

The answer is yes, mostly because the financial

United Rentals has acquiredUS rental companyNational

Pump &Compressor for a price of US$780million,

equivalent to 3.7 times National’s 2013 revenues.

Was it a good deal, andwhat does the pricemean

for the industry? Jeff Eisenberg reports.

SOURCES: 2013 figures fromUnitedRental’s press release, 2014 and later estimates by the author.

1200

1000

800

600

400

200

0

Revenue

EBITDA Debt

Valuation net of Debt

2013

2014

2015

2016

2017

2018

ANational Pump trench bypass project. The company

has 35 locations, including four in Canada.