FINANCE

14

CONSTRUCTION EUROPE

SEPTEMBER 2014

RESERVE CURRENCIES

Beginning

End

Change

Change

of period of period

(%)

British Pound

0.7939

0.8009

0.0070

0.89%

Japanese Yen

137.88

137.84

-0.03

-0.02%

Swiss Franc

1.2142

1.2100

-0.0042

-0.35%

US Dollar

1.3609

1.3283

-0.0326

-2.40%

EUROPEAN CURRENCIES

British Pound

0.7939

0.8009

0.0070

0.89%

Bulgarian Leva

1.9558

1.9559

0.0001

0.01%

Czech Koruna

27.431

27.766

0.335

1.22%

Danish Krone

7.4555

7.4553

-0.0002

0.00%

Hungarian Forint

310.28

313.74

3.47

1.12%

Norwegian Krone

8.3799

8.1597

-0.2202

-2.63%

Polish Zloty

4.1431

4.1820

0.0389

0.94%

Romanian Lei

4.4178

4.4034

-0.0144

-0.33%

Swedish Krona

9.2087

9.1613

-0.0474

-0.52%

Swiss Franc

1.2142

1.2100

-0.0042

-0.35%

Period: Week 28 - 34

Index

Beginning

End

Change

Change

of period of period

(%)

CEE (Equipment)

260.19

261.36

1.18

0.45%

CEM (Materials)

162.82

157.39

-5.43

-3.33%

CEC (Contractors)

192.88

185.41

-7.48

-3.88%

CET (Total)

200.14

196.23

-3.91

-1.95%

Dow

16915

17039

124

0.74%

FTSE 100

6687

6783

96

1.43%

Nikkei 225

15164

15539

375

2.47%

CAC 40

4323

4290

-33

-0.77%

DAX Xetra

9670

9413

-257

-2.66%

Period: Week 28 - 34

VALUE OF €1

KEY INDEXES

Summer slowdown

August saw confidence in the European

construction sector remain positive,

according to the

CE

Barometer survey,

but some aspects of sentiment have

come off the boil thanks to the

holiday season.

The overall climate of the August

survey remained strong, with

a positive balance of 22% – an

almost identical result to July. The

balance figure is the percentage

of positive responses, minus the

number of negative ones, so a figure

like +22% for the overall climate is a

strong indicator of positive confidence.

However, digging into the data revealed some interesting views

about where that market strength comes from. By far the most

strongly positive views were about the future, with a balance of

+37.3% of respondents saying they expected activity levels to be

higher in a year’s time compared to now.

There was also a very clear view that the market had improved

compared to a year ago, with +22.9% of respondents saying they

were busier this August than 12 months ago.

However, there was a sharp dip in month-to-month work, with

a balance of just +5.9% of respondents saying they were busier in

August than July. This measure of sentiment has been comfortably

above +10% all year, and at times has been as high as +25%.

This may not be anything to worry about. The

CE

Barometer often

shows a fall in activity over the height of summer, and this is usually

followed by a rebound in September and October.

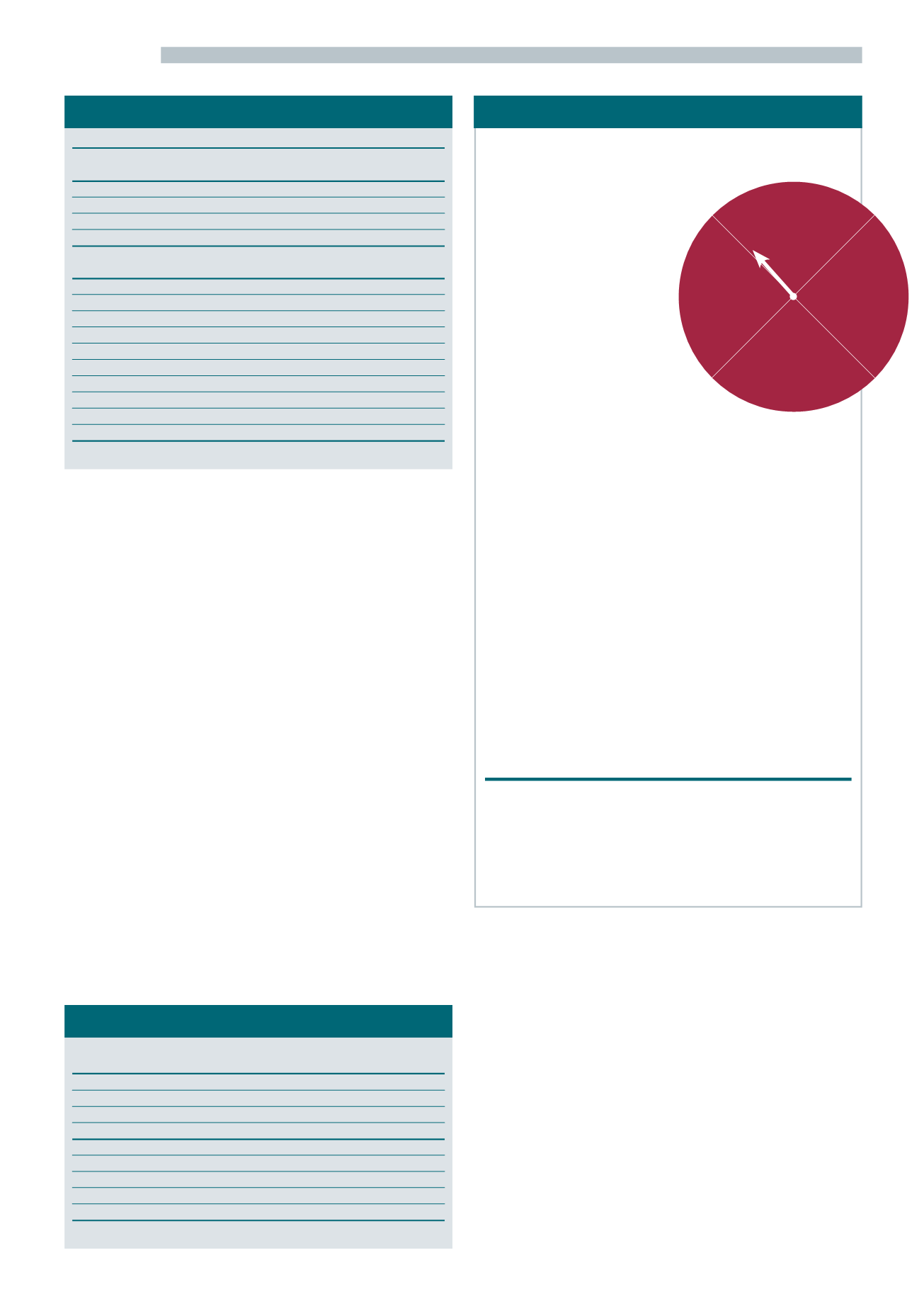

This is illustrated by the clock diagram, where the strong sentiment

about the future, but low current activity levels indicates an

upswing on the horizon. The clock indicates only which way the

market is heading, and how many people share that view – the

length of the arrow is the strength of the sentiment. It does not

indicate how big market growth might be.

ce

CE

BAROMETER

like Caterpillar and Deere saw

their share prices fall between

weeks 28 and 34, as was the

case for smaller companies

like Astec, Manitowoc and

Terex.

Many of the gains in the

sector came from the Japanese

manufacturers, with Hitachi,

Kobe Steel, Komatsu, Kubota and

Tadano all up.

There

was

also

good

support from the European

manufacturers, led by Metso’s

21.82% rise, which was driven

by good half year results and a

TAKE PART

The survey, which takes just a one minute to complete, is open to

all construction professionals working in Europe. The

CE

Barometer

survey is open from the 1st to the 15th of each month on our

website.

■

Full information can be found at

R

E

C

E

S

S

I

O

N

B

O

O

M

U

P

T

U

R

N

D

O

W

N

T

U

R

N

has not lowered interest rates as

much as other central banks, or

embarked on quantitative easing.

However,

with

Europe

continuing to look decidedly

behind the pace in terms of

its economic recovery and the

threat of deflation mounting, the

currency may weaken anyway

and should certainly go down if

the ECB starts printing money.

Fortunes in the Eurozone are

also likely to affect stock markets,

as its troubled currency and the

questions raised by the Banco

Espirito Santo affair are among

the chief economic worries at the

moment, alongside the West’s

relationship with Russia and

unrest in the Middle East.

ce

bold strategic announcement in

which the company said it would

shift to a more services-oriented

business model.

CURRENCIES

Poor economic data for the

Eurozone and deflation concerns

saw the Euro lose ground to

the Japanese Yen, Swiss Franc

and US Dollar between weeks

28 and 34, with the biggest fall

being 2.40% against the Dollar.

It also lost some ground to other

European currencies, but was up

against the British Pound and a

few others.

The Euro has been relatively

strong since before the financial

crisis, partly because the ECB

The Euro has been relatively

strong since before the

financial crisis, partly because

the ECB has not lowered

interest rates as much as other

central banks, or embarked on

quantitative easing

prices fall, with Cimpor and

Italcementi suffering the most.

The only companies to see a rise

over the six-week period were

Kone, Saint-Gobain andWolseley.

However, it was a different story

for equipment manufacturers,

with the CEE Index managing a

modest 0.45% gain over the same

period.

Although one might imagine

this was because of the number

of US companies in the Index

following the upward trend of

the Dow, this wasn’t the case.

Big capitalisation US players